Three killers sentenced to life in prison

THREE vengeful thugs responsible for the “senseless and savage” killing of an innocent party-goer in a South Yorkshire street have been jailed for life.

Richard Wray, aged 38, and Adam Richards, 24, were yesterday handed life sentences after being found guilty of murdering Shaun McDermott following a trial at Sheffield Crown Court last year.

Wray’s son Lewis, aged 17, also convicted of murder, was remanded into Her Majesty’s pleasure – which the judge said was the youth equivalent of a life term. They were among an “armed to the teeth” gang who leapt out of a van and attacked the Bentley joiner in Welfare Road, Woodlands, on June 25, last year – after they mistook him for somebody else.

Mr McDermott was knocked out and beaten as he lay on the ground.He was then stabbed in the heart and died later that night in Doncaster Royal Infirmary. The defendants were sentenced to a total of at least 37 years behind bars.

Richard Wray, of The Crescent, Woodlands – said to have wielded the knife – was jailed for a minimum of 15 years.

Adam Richards, of Tudor Road, Woodlands, who prosecutors said knocked Mr McDermott out at the beginning of the attack, was ordered to serve at least 13 years.

Lewis Wray, of South Street, Highfields, who had no previous convictions, was handed a minimum sentence of nine years in custody.

01 February 2006

Mr. Toad’s Wild Ride

[Note: This was intended to go up yesterday morning, but I was unable to post due to small, now resolved, technical difficulties. So, before anyone tells me that the Nikkei closed slightly down today, I know, I know.]

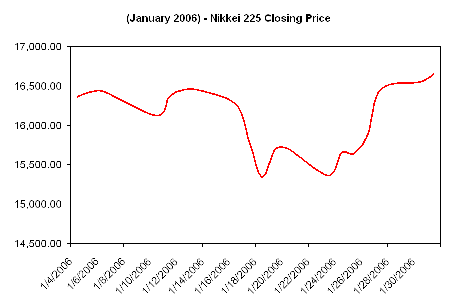

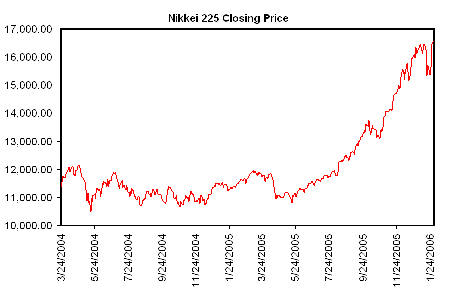

Even though this post has nothing to do with toads or amusement parks, I chose the title in keeping with the anurian theme of this blog. But boy, wouldn’t this month’s Nikkei 255 make one hell of an exciting coaster ride?

I smoothed the line just for a more pleasing visual effect, but the bounce back from the “Livedoor Shock” is clearly official. In fact, for the past two days the Nikkei 225 average has closed at highs not seen since September 2000.

Lacking the sophistication to explain the reasons behind this (and having had it correctly pointed out to me over the weekend that I am wont to jump to unsupported conclusions about Japan) I’m going to defer to the opinion of the “professionals” on interpreting this one.

Analysts are citing several factors for the latest rally.

First, a number of positive economic indicators appear to have improved the confidence of investors. Starting with the labor market, employment data for December showed a marked improvement, with the ratio of job offers to job seekers balancing out at one to one, the highest it’s been since September 1992. The unemployment rate fell an additional 0.2 percent, to 4.4. percent, the lowest level in seven years.

Housing figures also look promising. Starts in 2005 rose for the third strait year, up 4% to 1,236,122.

Industrial production also rose by 1.4% (seasonally adjusted) in December.

Finally, gains by individual companies also seem to have played a roll. A fall in the yen-dollar exchange rate has been a boon to profits of exporters such as Toyota, Honda and Advantest, all of whom closed higher on Tuesday.

Meanwhile, rising oil prices equal increased profits for companies like Nippon Oil and AOC Holdings, Inc.

Looked at as a whole, all of these figures (except perhaps for the higher oil prices) appear to suggest movement towards a stronger economy – higher corporate profits, more hiring, and increased private consumption and spending.

But, while those factors are fine for institutional investors who have the resources to pay anti-social quant jocks to stare at computer monitors all day while mentally multi-tasking the application of Einstein’s general theory of relativity to global securities markets, what about individual investors? I’m talking about the average Tanaka on the street, punching trades into his cell phone?

Well, in my humble, albeit relatively uninformed opinion, these guys might be basing their investment decisions on this:

Now, aren’t you sorry you didn’t buy in last May?

Police take on pirates in fake alien frog showdown

Sorry, but it’s all downhill from the headline. It’s not that it’s a bad article exactly. Something about how the new Japanese cartoon Sergeant Keroro (ケロロ軍曹-main character pictured at left) has gotten so popular that toys modeled after the character are being bootlegged, and the anime downloaded illegally all over Taiwan and China. Ok, fine, interesting to know I guess-although seriously, by now wouldn’t you expect the same thing to happen with any even halfway popular cartoon show? I mean, after that headline I was really hoping for something with a little more juice than a story about toy pirates.

Sorry, but it’s all downhill from the headline. It’s not that it’s a bad article exactly. Something about how the new Japanese cartoon Sergeant Keroro (ケロロ軍曹-main character pictured at left) has gotten so popular that toys modeled after the character are being bootlegged, and the anime downloaded illegally all over Taiwan and China. Ok, fine, interesting to know I guess-although seriously, by now wouldn’t you expect the same thing to happen with any even halfway popular cartoon show? I mean, after that headline I was really hoping for something with a little more juice than a story about toy pirates.

Ah well. If you’re curious, you can download bootlegs of the show from this anime fansubs bittorrent site. I’ve seen a few minutes here and there on Taiwanese TV, and while I couldn’t really tell what was going on, what with it being in Chinese and all, it did look pretty funny.

Japan’s hidden arms trade

With all the debate over a possible constitutional revision in Japan aiming towards formal remilitarization (of course their informal military is already among the world’s best equipped), there have been quite a few mentions of how Japan’s current constitution is so limiting that it actually blocks Japan from collaborating with the US in constructing a missile defense shield in Japan. This is supposedly due to Japan’s ban on the export of arms, so you might be forgiven for actually believing that Japan doesn’t sell weapons to other countries. This article at Asia Times (originally from Japan Focus) explains the technicalities and blurry definitions that the Japanese government exploits to enable a continuation of their claim that they do not trade in weapons, while still being able to profit by selling small arms all around the world.

Japan actually conducts a thriving small arms export trade. The international annual publication, the Small Arms Survey, for example, reported that in 2002 Japan exported $65 million worth of small arms which, in monetary terms, ranks Japan among the top eight exporters of small arms worldwide for that year. [8]

The Japanese government evades this issue by contending that “hunting guns and sport guns are not regarded as ‘arms’,” [9] and therefore the self-imposed ban on arms exports only applies to guns of a military specification. This raises the question of what differentiates a military specification gun from a sporting or hunting weapon. However, the Japanese Ministry for Export, Trade and Industry (METI) provides no comprehensive definition. Instead it decides on a case-by-case basis whether a weapon should be defined as being of military specification.

This is another example of saying one thing and doing another, much in the same vein as the policy of promoting commercial whaling in the guise of “science” while still being party to a treaty outlawing commercial whaling, as I discussed a few days ago. Unlike the whaling hypocrisy, the open secret of Japan’s international weapons trade seems to have remained completely beneath the radar. While I have in the past been slightly confused by references I’ve seen to Japan-manufactured guns, until I saw this article I just shook off the momentary bafflement without realizing the actual situation. A highly recommended read.

The “what the hell” theory of Japanese law

Unless you follow the business media in Japan, you probably haven’t heard about the upcoming overhaul in Japanese corporate law. It’s pretty intense, and it illustrates my personal favorite theory of Japanese legal policy: the What The Hell Theory. Basically, the theory states that:

- Japan sees a legal instutition overseas and decides to adopt it.

- Japan picks a random portion of the institution and says “What the hell! Let’s change it!”

- This change leaves Japanese society with an evil mutant form of a foreign institution that doesn’t really work properly.

Case in point: this new institution called the godo kaisha (GDK). Up until now, there have been two basic kinds of corporations in Japan: the kabushiki kaisha (KK) and yugen kaisha (YK). The YK structure is for small companies, and the KK structure is for large companies (or, more often, small companies that want to seem large). As of April, the YK will cease to exist and its place in the system will be filled by the GDK. Continue reading The “what the hell” theory of Japanese law

Takebe’s Grandchildren Think Horie is His Brother… OOPS!

At a speech in Saitama City, the embattled LDP Secretary General Tsutomu Takebe, who is being blamed for his outpouring of support for ex-Livedoor president Takafumi Horie during the September 2005 Lower House election, let people know that he had to tell his grandchildren that he is in fact NOT Horie’s brother, despite saying so at a speech at the time.

Aso Backs off of Tactless Emperor-Visit-Yasukuni Speech PLUS

Tuesday, January 31, 2006

Aso Qualifies Remark Calling For Emperor To Visit Yasukuni

TOKYO (Kyodo)–Foreign Minister Taro Aso clarified Tuesday that his call over the weekend for the emperor to visit the war-related Yasukuni Shrine in Tokyo was not meant for the emperor to go there ”in the current situation.”

”I made the remark from the standpoint of the spirits of the war dead enshrined (at Yasukuni) because they died for the emperor. I never said that (I wanted) the emperor to make the shrine visit in the current situation,” Aso told a news conference.

Aso said Saturday in a speech in Nagoya that ”From the viewpoint of the spirits of the war dead, they hailed ‘Banzai’ for the emperor — none of them said long live the prime minister. A visit by the emperor would be the best.”

Nothing witty to say about this guy, but I have discovered a wonderful site dedicated to the man. This site is as fascinating as it is jam-packed with information. Some quick highlights:

Continue reading Aso Backs off of Tactless Emperor-Visit-Yasukuni Speech PLUS

Why I’m changing my name, part 1

I’m taking an overnight trip out of town in a couple of weeks, and I decided to book a room in a “business hotel” online. Some of these places are surprisingly cheap: you can stay in the middle of a big city for as little as $40 a night or even less.

Then, I got this email:

Thank you for your reservation at ____ Hotel. We are contacting you because of a matter of importance for our customers from overseas.

At ____ Hotel, our rooms are secured at night with an automatic lock system and PIN pads. While the PIN pad system is very convenient, it is also complicated, and among our customers who are not particularly proficient in Japanese or have difficulty understanding Japanese, many have been unable to use the system, or have been locked out of their rooms at night.

Because of this, we ask all customers who do not speak Japanese to provide a translator at check-in when possible. After one stay the system is fairly easy to use, but as we cannot verify that you, Mr. Joe [sic], have stayed with us before, we are sending this message to you. Thank you for your understanding and cooperation.

Yet another reason I need to naturalize and change my name to Joichi Koizumi.

Update: I was thinking about this over a slow afternoon in the office, and I started wondering: “What would Debito do?” (Somehow he works his way into all of my blog posts.) So I wrote back to the hotel:

Thank you for your e-mail. I live in Japan and work as a translator, so I don’t think there will be any problem. One thing I do wonder about, though, is whether you have had instructions written in English? Many hotels and weekly mansions in Tokyo have similar systems, and they provide instructions in English so that foreign customers do not have to worry about misunderstanding. Maybe something similar would save you from having to send out these warnings (and also be more convenient for your guests who don’t speak Japanese).

The hotel manager wrote me back within ten minutes.

Thank you for your reply. We do indeed have an English version of the instruction sheet you suggested in your e-mail, so please don’t worry about that. Our customers are not generally from the English-speaking world, thus the e-mail you received. Thank you again for your comment, and we hope you have a safe trip.

Sooo, that’s that. I guess the interpreter is only necessary if you can’t read.

Birthday cigarette [photos]

Larger size here.

Larger size here.

Taken December 28, 2005 at a friend’s birthday party. The red glow comes from the focus assist light of someone’s miniature digital camera. I was looking through my camera while they took a photo, and when I saw the appearance of the scene bathed in orange light I had them keep it trained on the subject while I took my own photos.

Both taken with Canon 300D and 17-85mm EF-S lense.

Kujira versus Echizen

No, it’s not the title of the newest Godzilla spinoff, but the stars of the two recent seafood related news stories that have been making waves in Japan.

I’ll start with kujira, which is the Japanese word for whale. Japan has not just continued it’s program of so-called “scientific whaling,” in which they violate the international treaty prohibiting commercial whaling while pretending they haven’t, but is actually increased their catch. This is despite the fact that almost nobody actually likes whale meat.

According to the report, the inventory was about 1,000 to 2,500 tons around 1995. It hit a low point of 673 tons in March 1998 but began to increase to reach 4,800 tons last August.

[…]

The Fisheries Agency admits the whale meat inventory is rising and has begun studying ways to expand sales in Japan.“It is true that such a trend exists. We will study ways to expand sales channels as well as to reform sales methods,” an agency official said.

Such moves by the government to stimulate the whale meat market will probably draw more criticism from antiwhaling groups that fear more consumption in Japan.

Since 2000, the research whaling has been expanding in terms of volume and number of species. On the other hand, consumption has not increased as areas of high demand for whale meat are limited in Japan.

“Unless the consumption of whale meat increases dramatically, the stockpile of whale meat will surge,” Sakuma said.

I’m not interested in getting into the debate over whether or not commercial whaling should be allowed, but irrelevant to that argument I can say that this current policy is just absurd. While Japan has been making some progress in their battle to change the treaty banning commercial whaling, they have, in fact, signed a treaty banning commercial whaling. They are, in fact, violating that treaty while pretending not to. The fact that Japan is carrying out their whaling operations illegally only makes it easier for opponents of whaling to continue to attack them by adding the illegality of it to the moral/environmental argument, in contrast to Noraway, who carries out fully legal commercial whaling by virtue of having never signed the anti-whaling treaty.

Echizen (actually echizen kurage) are a species of massive (200kg) but benign (as in, they aren’t the stinging kind) jellyfish that have recently been multiplying like crazy in Chinese and Korean waters, and drifting towards Japan in plague-like proportions. There are so many of these gigantic blobs floating around the Sea of Japan that it has actually become impossible for fisherman to put out their nets without catching some, sometimes to the point where catching actual fish becomes almost impossible.

South Korean fishermen have been suffering similar woes, but China, where giant jellyfish are a delicacy often served dried and dressed with sesame oil, does not seem to have registered the outbreak as a major problem, Japanese officials said.

Seaside communities in Japan have tried to capitalize on the menace by developing novel jellyfish dishes from tofu to ice cream, but for some reason the recipes have failed to take off.

Participants at Thursday’s conference said they had experimented with feeding the jellyfish to farmed crabs and using them as fertilizer.

What we have here are, basically, are two different sources of sea-borne protein, and neither one is even remotely popular or has much of a market. One form of protein is for some reason being pursued with vigor despite the fact that doing so leads to both international controversy and such a massive excess of the stuff that it ends up just rotting (or at least staying frozen) in warehouses.

What we have here are, basically, are two different sources of sea-borne protein, and neither one is even remotely popular or has much of a market. One form of protein is for some reason being pursued with vigor despite the fact that doing so leads to both international controversy and such a massive excess of the stuff that it ends up just rotting (or at least staying frozen) in warehouses.

The second form of protein is also in no particular demand as a food source, but it is so abundant that it is literally washing up on the shores of Japan and clogging the nets of fishermen.

Japan’s commercial whaling is a diplomatic and economic failure, and all the resources being spent by the government in supporting it are a complete and utter waste, serving no purpose except to satisfy a nostalgic fantasy of older people who remember eating whale meat in the school lunches in the years after the Second World War when far more desirable meats like pork or beef were difficult to come by.

The sea is so thick with echizen jellyfish that catching some is unavoidable, and therefore figuring out how to exploit them as a resource is an economic necessity in areas where the fishing industry is disrupted. From a purely market based standpoint, an increase in the catch of unwanted whales is absurd, and the slow pace of developing echizen into a positive resource is wasteful in another way.

The sea is so thick with echizen jellyfish that catching some is unavoidable, and therefore figuring out how to exploit them as a resource is an economic necessity in areas where the fishing industry is disrupted. From a purely market based standpoint, an increase in the catch of unwanted whales is absurd, and the slow pace of developing echizen into a positive resource is wasteful in another way.

As stocks of wild fish are becoming depleted in some areas, the farming of fish is becoming steadily more popular. But to support fish grown in farms, they still have to send out trawlers to catch huge hauls of smaller fish species to use as feed, so even though they aren’t catching as many, let’s say salmon or tuna, they may still be depleting the species that those fish survive on in the wild. Perhaps the echizen, which naturally are more abundant than ever, could be become a primary source of protein for farmed seafood, and by extension, the humans who eat them.