I ran across this while perusing the Federal Government’s job website. I think i might be a little underexperienced with a cleaver for this one, but I know somewhere out there, someone will see this and think to themselves, “I am so qualified for THAT!”

MEATCUTTING WORKER / MEATCUTTER

Salary Range: 28,028.00 – 44,265.00 USD per yearJob Summary:

Consider the rewards that this challenging opportunity may provide. In this position, you may supervise, lead, assist, or perform work involving cutting, trimming, and removing bones from meat and preparing and processing fish and poultry. This includes cutting meat into steaks, roasts, chops, cutlets, ground meat, and other small cuts, using powered equipment such as meat saws, slicers, grinders, and hand tools such as meathooks, knives, saws, and cleavers. A great opportunity is just a click away ? apply now.

And, if Japan ain’t your thing, how about beautiful Guam?

MEATCUTTING WORKER

Salary Range: 10.20 – 19.48 USD HourlyWork Schedules: May be part-time ( 16-32 hours per week ), intermittent ( work on an as-needed basis ), or full-time ( 40 hours per week ).

Major Duties: The work involves cutting, trimming, and boning meat, fish, and poultry using hand tools and operating power meatcutting equipment. Receives instructions on work to be done and the tools and equipment that will be needed. Through day-to-day assignments, Meatcutting Worker becomes skilled in standard meatcutting techniques and broadens knowledge of established methods of processing assigned cuts.

Qualifications: To meet the screenout for this position, applicants must show they have the ability to do the work of Meatcutting worker without more that normal supervision. Examples of experience that would indicate this ability is Basic knowledge of the muscle, seam, and bone structures of different kinds of animals, the ability to learn methods of processing meat when given detailed instructions; and skill in using hand tools such as knives, scrapers, and handsaws.

Education Requirements: There are no minimum education requirements for this position.

“Basic knowledge of muscle, seam and bone structures of different kinds of animals?”

I wonder what kind of people this type of job attracts? Are there people out there who aspire to this kind of work because they are actually passionate about muscle, seam, and bone structure?

I am not poking fun (well, not too much anyway) but am genuinely curious. I never even knew “meatcutter” was a job title, but as of 10:01 am EST on 02/17/06 there are nine meatcutting jobs available with the Federal Government alone. Has anyone out there ever done this type of work and would be willing to share their experiences in the comments section?

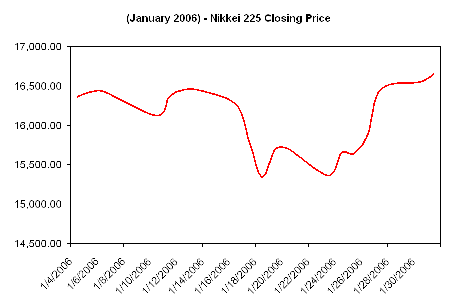

(Source: Washington Post)

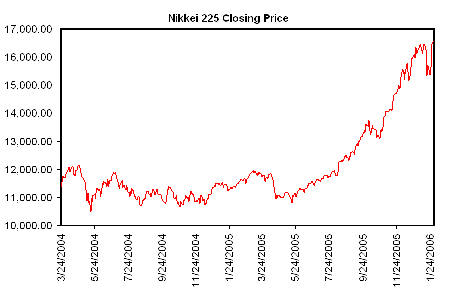

(Source: Washington Post)